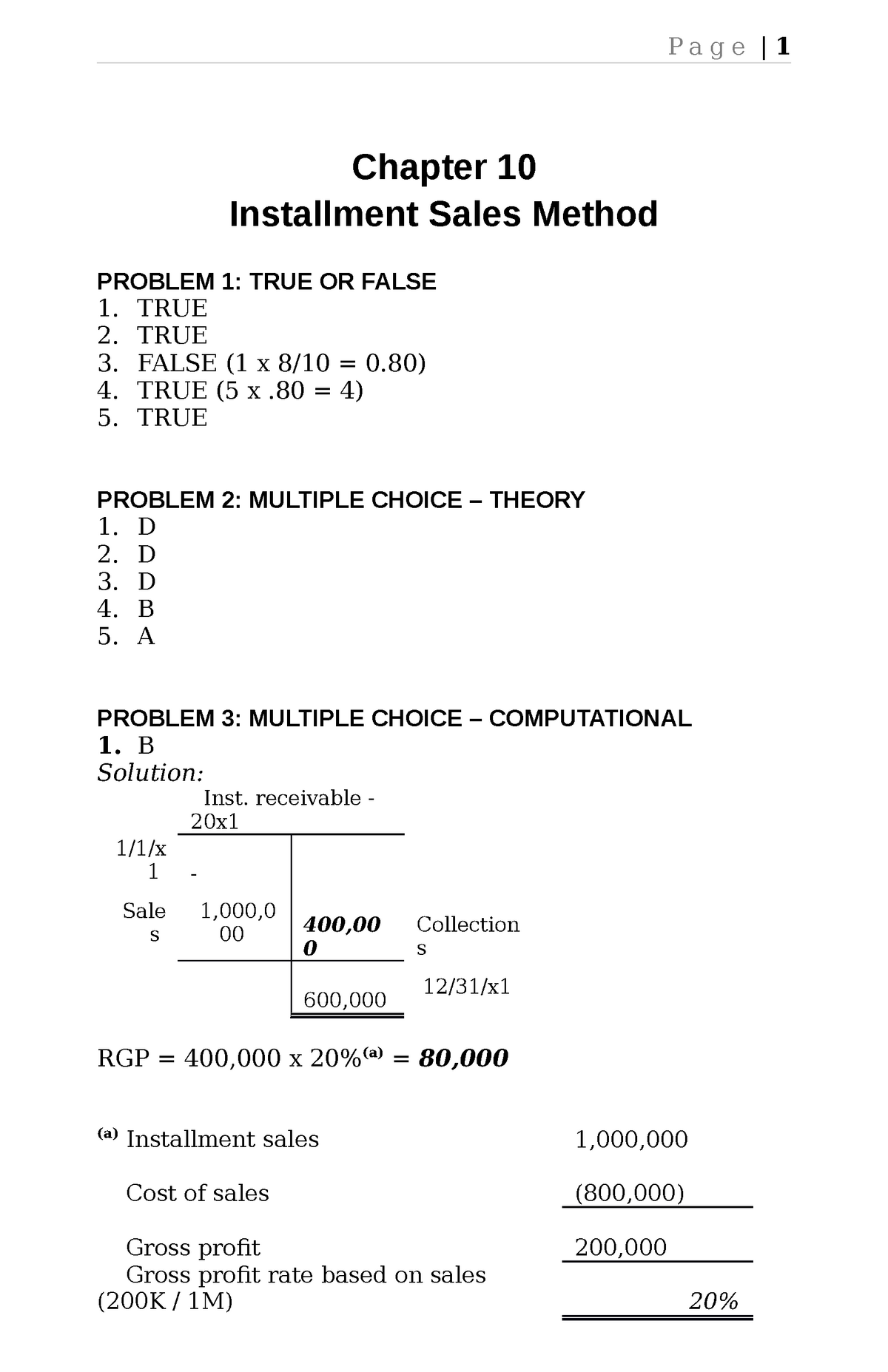

- Your own residence’s market value was $eight hundred,000

- Your existing financial balance try $2 hundred,000

- The newest maximum. cash-aside amount borrowed are $320,000 (80% x $eight hundred,000)

- Your maximum. cash-back is actually $120,000 ($320,000 – $two hundred,000)

Merely Va finance (mortgages to have veterans and you will services participants) enable you to perform an earnings-away refinance by which you’re taking aside 100% of your own guarantee.

You are not using the the latest mortgage to settle your current that. Nevertheless first mortgage and you can second home loan joint always can’t be significantly more than 80 per cent of residence’s value. So the mathematics ends up an equivalent.

But not, certain household guarantee loan companies are more versatile and can succeed you to use doing 85 per cent of the home’s value.

How to make use of the finance

Although not, you usually want to use the money to have some thing which have good a beneficial profits on return. That is because you’re paying interest toward bucks and it’s really shielded by your domestic.

Prominent ways to use domestic guarantee include domestic home improvements and you can debt consolidation reduction (making use of the currency to settle large-appeal personal loans or personal credit card debt).

Residents can be in a position to subtract the interest towards the very first $750,000 of one’s new mortgage should your bucks-away financing are accustomed to create money developments (in the event since a lot fewer someone today itemize, most properties wouldn’t take advantage of so it develop-off).

Today, we aren’t taxation advisers. Which means you has to take your recommendations of a specialist just before counting on you to definitely guidance.

Nevertheless tends to be that you can so you can subtract having investment property on the renovations. Very give it a try if that’s precisely why you want to acquire. As it might be a definitive factor in your personal household guarantee financing against. financial study.

Reduced currency if you need to security pandemic expenditures

By the way, government regulator the consumer Financial Protection Bureau just last year caused it to be faster to view financing thanks to cash-out refinances and you may HELs if you want money urgently to pay for pandemic-associated expenditures. If this pertains to you, consider this.

When to use a mortgage more than property security loan

Going for a money-out re-finance more than a home guarantee mortgage are a beneficial means to fix keep your monthly expenses lowest. Remember that money are typically lower once the you’re simply spending one to home loan as opposed to a couple of.

A cash-away refinance is also the higher alternative if you want to refinance in any event. Assume your mortgage rate is 4% nevertheless you’ll refinance to an excellent 3% one to. Might reduce your monthly premiums. As well as your coupons manage in the near future pay money for your closing costs.

Obviously, if you take big money out together with your refinance, you might still have a high payment per month. But you’ll have that lump sum, too. And do just about anything you love towards the finance, just as with property equity mortgage.

When to explore a house collateral loan unlike home financing

A property guarantee loan is usually a far greater solutions than simply a great cash-aside re-finance when your newest home loan is virtually repaid, or you already have an ultra-lowest mortgage price.

Because of the choosing a beneficial HEL, you could potentially faucet their equity versus stretching the word otherwise changing the speed in your current financing.

You might like to pick a house security financing for those who can afford increased monthly payment and want to save your self much more ultimately. Remember that a beneficial HEL will likely cost more week-to-few days – however you will pay it off much prior to when a finances-out home loan.

Additionally, you will save well on settlement costs. And you may, as the interest rate you have to pay tends to be large, the reality that you are borrowing faster for a smaller months typically setting you’ll end www.paydayloancolorado.net/mulford/ up best off across the continuous.