Among the many simple questions are, were there certain abusive practices that truly is going to be away from probably the thought of a trigger? You’ve got named a few of them. Therefore we do show your own consider that there is a would like to handle that it when you look at the a blended means, much more performs from the a number of the companies at this new table in controls and you will enforcement, also an innovative new glance at the regulations.

However they are talking about fund

Ms. SEIDMAN. I’d go along with what Assistant Gensler has said and in sort of, the problems away from turning, the lead to and you can borrowing existence that are some thing I think are considerably into side burner for everyone.

I would personally also should build into the one thing the Comptroller said prior to, which is which entire dilemma of examination. I’m sure a few of the Claims do an adequate job and are in there performing reports of your own home loan bankers and you may lenders who happen to be susceptible to its jurisdiction. All of us need to make sure we have fun with one unit to the maximum the amount you’ll be able to.

Mr. MEDINE. On the problem of HOEPA triggers, I believe its definitely worth the committee’s idea. Wisconsin personal loans I’ve examined loan providers for the past few years and located he has carefully left the loans slightly below the new HOEPA cause to be able to avoid the very important defenses you to definitely HOEPA provides consumers.

Our certain recommendations is that the items which might be billed users?borrowing lifestyle, handicap, auto insurance, vehicle nightclubs?all be as part of the HOEPA pricing to ensure that is not a new type to stop those very important protections.

Mr. CELLI. Into the County peak, I think there’s an archive already of trying to deal with many different of one’s facts your elevated. Nine Says possibly provides enacted statutes, explore current regulating expert, or is looking for Condition top laws. In my opinion one to checklist is really full and one you to definitely almost every other County height regulating bodies and you will legislatures are exploring.

Mr. LAFALCE. I’m not Bill Safire, but I really do have some concerns for the use of the English vocabulary, thus i need their help.

When i think about a primary financing, I think of just one material. Easily think that I would like to shell out something over a prime?otherwise over finest?that’s things; basically should shell out some thing below the top, which is another thing also. Usually I would like best or something lower than the top and i also would label things less than the prime subprime. Therefore everybody is talking about subprime funds, however, men and women was highest-costs loans. Isn’t that an incorrect use of the English words? Cannot i feel speaking maybe on the subprime individuals? Shouldn’t i eliminate the utilization of the phrase ”subprime loans” whenever we’re writing about significantly more than primary loans? Assist me, please.

In the a third of your consumers got results over 620, which is basically the Fannie/Freddie cutoff having an one quality loan

Mr. HAWKE. Mr. LaFalce, contained in this context, the definition of ”prime” does not reference the top rates as a result, but on top-notch the financing.

Mr. LAFALCE. They use the term primary and you will financing inside the exact same perspective, create it perhaps not, the one before other, the definition of finest until the word mortgage then they normally use the definition of subprime up until the phrase loan. That is what brings me difficulty. In my opinion we are flipping this new English words to your the head plus it bothers myself.

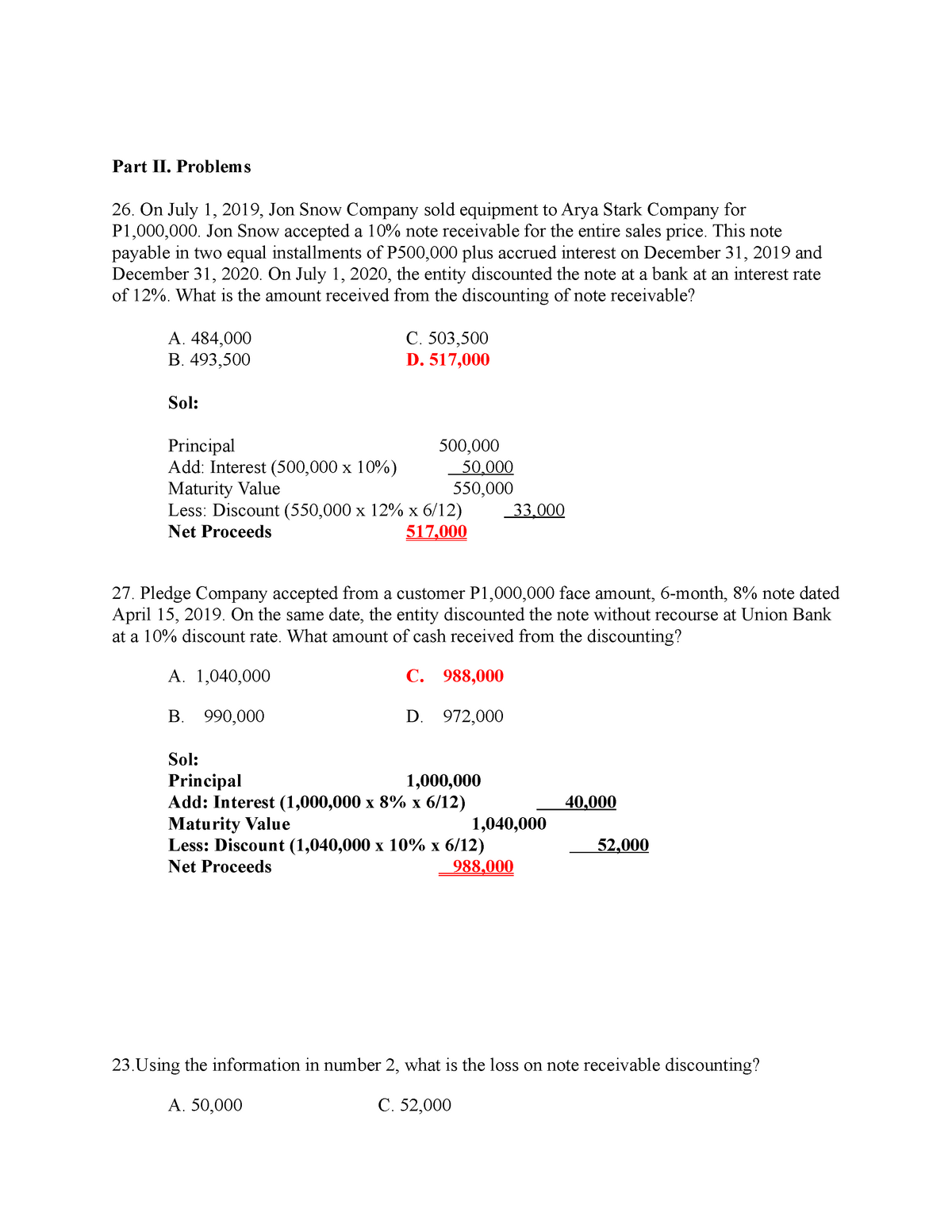

Ms. SEIDMAN. I want to mention, because the Under-secretary Gensler talked about, not all the subprime loan holders is subprime borrowers. I’ve has just looked at the borrowed funds Suggestions Corporation data, that’s a highly complete databases away from subprime money.