And be sure to see used cars. Capable sometimes render at a lower cost. Just make sure that in the event that you funds good used car, don’t exercise as a result of short care about-financed used car investors. They can charges exorbitant rates of interest.

Although you cannot in fact place an asking price on what you acquire of a college degree, there clearly was undeniable proof you are rather better off financially having a college degree. Interest rates to the government student money are often quite low. Very once again, you have made something of value on a low interest.

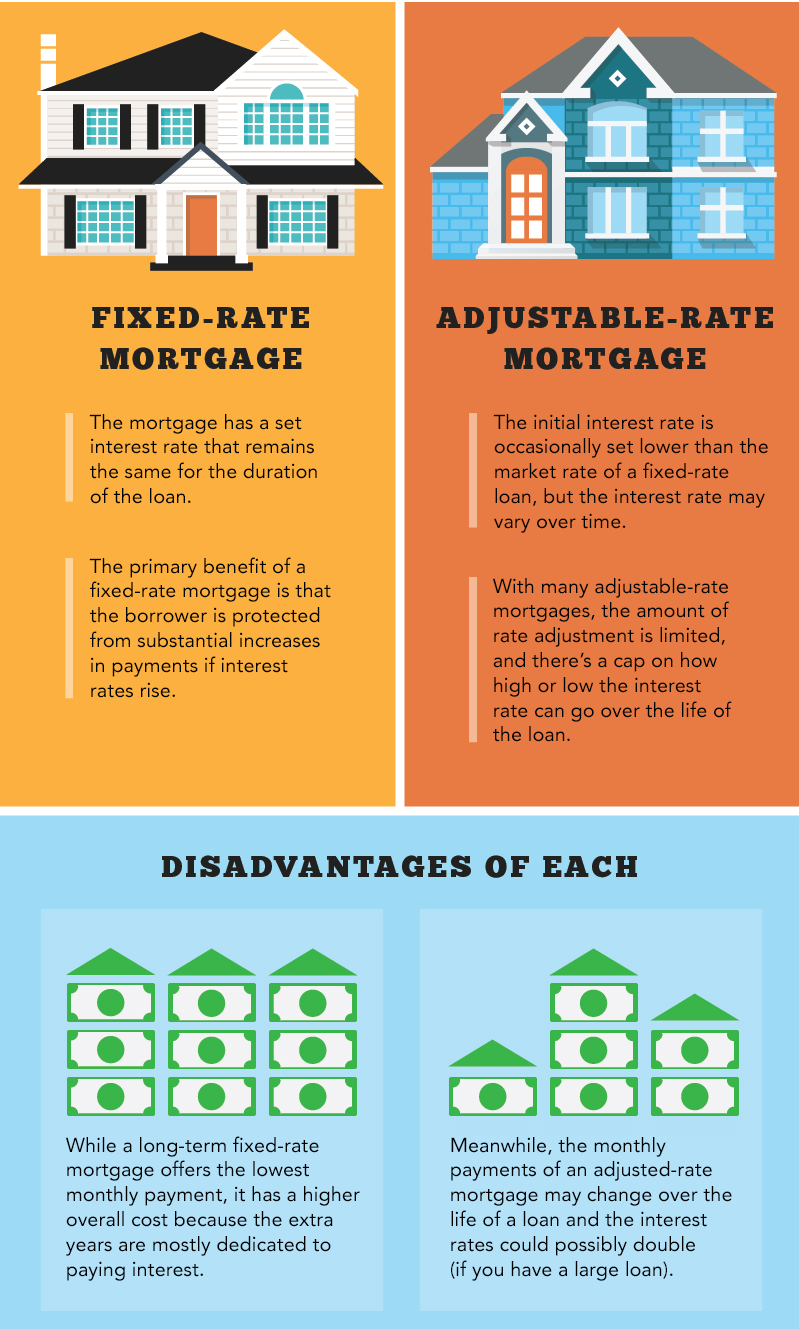

Given that a side note, particular target=”_blank”>condition and private money have really serious restrictions regarding payment, price decrease and forgiveness, so they are able commonly fall into the fresh crappy personal debt category.

The better the fresh Annual percentage rate, the go to the website bigger the fresh new amount of money you might be sending so you can the lender per month

And at the bottom of new pile try credit debt. Credit card debt is sold with higher notice, always around 15% to help you 17% and generally pays for points that hold no built-in worthy of (eating, flick seats, alcohol, footwear…). It will make nothing financial feel to take credit debt. Stop carrying personal credit card debt as much as possible.

If you’re the financial institution, a leading Apr is terrific, due to the fact you might be one getting the desire

At the base of the base is payday lenders. It costs higher interest and you will charge, and their subscribers score trapped during the never ending loops regarding quick-identity funds. Remain far, at a distance from the variety of financing.

What exactly is an apr? For a lot of the word Apr normally send a-shiver down the spines… What is so terrifying? Annual percentage rate signifies Apr, and you will signifies the price of attract and costs charged because of the a great lender towards a fantastic financing. For people who are obligated to pay a great deal on the mastercard, Apr is really a frightening topic.

Different kinds of fund will have some other quantities of Annual percentage rate. Generally, the latest riskier the borrowed funds, the greater new Apr. When you features a bad credit rating, loan providers often ask you for high prices while they imagine your high risk.

Down cost apply to finance which can be secured, or features property attached to all of them. Therefore auto loans otherwise mortgage loans will often have reasonable APRs, since if things lose their freshness, their lender can still get back your house or automobile. But consumer debt, including personal credit card debt, is much more challenging to gather in the event the some thing go south, since there is no house linked to the mortgage. These types of money possess high APRs.

However, Apr can be your buddy too. Bring your family savings for example. This really is a generally that loan you will be making into bank. They then take your deposit and you will provide your finances out to anyone else. For this right, your bank will pay your attention, or an apr. Unfortunately, now in the long run, once the rates are so reduced, the fresh Annual percentage rate your own bank provides you with was extremely lowest.

Something you should look for is an activity titled an enthusiastic APY, or Yearly Payment Produce. A keen APY takes the power of compounding into account. Into bank account, compounding occurs when you have made interest for the focus you’ve already earnedpounding ‘s the power on which money runs. If you rating a great 5% Apr, that’s made available to your monthly, you can acquire compounding to the notice your already made, throwing your own 5% Apr so you’re able to an authentic 5.11% APY gained. But end up being cautioned. If your bank estimates you an enthusiastic APY in your checking account, he or she is in reality making reference to the fresh compounded come back. The actual desire might give you each month might possibly be computed utilising the down Annual percentage rate! Sly!!